What does Ramaswamy's Roivant do?

Vivek Ramaswamy has been in the news as a rather controversial GOP candidate; His current wealth has been built in large part through his biotech company Roivant. So what does Roivant do?

Vivek Ramaswamy has been making the news due to a rather controversial political campaign. Of course, this has led to increased scrutiny of the ways in which he made his fortune: this include founding the biotech company Roivant. I must admit I had never heard of either Ramaswamy or Roivant before this campaign. But I’m interested in biotech & Roivant seems to be a rather unusual company. So naturally, I wanted to dig more into this, especially given claims I saw on twitter that his company is basically a “scam”.

So leaving politics aside, let’s look into what Roivant does. The first thing that stands out is that their unique value proposition is quite different from that of most biotech start-ups; It does not hinge as much on an innovative technology/platform, but rather on an innovative business strategy (for example their unique Vant structure). Instead of “engineering” things at the level of biology, they are engineering at the levels of financials/ops to make drug discovery more efficient1. This focus on financials is announced by the company name itself2: The “Roi” in the company's name stands for return on investment.

So how are they aiming to do that?

I think this bit from their S-1 filing is pretty good at capturing the core of their business model. Their core strategy is to in-license assets3 from larger companies. "In-licensing" in the pharmaceutical industry refers to a company obtaining rights to a product or technology from another company, typically in exchange for payments, milestones, or royalties. This allows the company to further develop, manufacture, and market the drug or technology without having originally discovered or developed it themselves.

Roivant’s bet is that it can leverage advantages in some key areas: improved decision making, specialisation through the creation of disease-area specific subsidiaries (so-called Vants) & a better incentive structure. This combination should allow it to “rescue” promising mid-to-late assets that have been discarded for various reasons by big pharma and bring them to market.

In-licensing assets is not new (indeed it’s a common practice), but building an entire company around it is. The other unusual thing about Roivant is that in-licensing usually happens on the part of larger companies who buy assets from smaller companies. This is because larger companies usually have the expertise and infrastructure to carry out the necessary Clinical Trials. By contrast, in this case, the incumbent, smaller company (Roivant) would in-license from the larger, established company.

How does this work?

Why would established pharma giants let go of assets they've already invested in? The answer isn't always straightforward. One primary reason can be business strategy. Imagine a company undergoing a strategic overhaul, deciding to concentrate its energies on certain therapeutic areas. In such a shift, they might de-prioritize entire disease categories, which means sidelining even assets that have shown potential.

Enter Roivant. They believe they’ve recognized a gap and are looking to capitalize on it. I think their strategy is grounded, at least in part, in the assumption that the pharma industry can be quite inefficient. These inefficiencies might stem from an array of reasons, from misaligned internal incentives to the cumbersome nature of bureaucratic decision-making processes. It's not always about the asset's potential but how it's perceived within the organisational structure. The idea that pharma makes bad decisions and exhibits bias, sometimes to the detriment of its own profitability and patients is not without merits. I really enjoyed Jack Scannell’s recent review discussing the use of improper decision making tools when prioritising targets in pharma. The same author's latest paper dissects the failure of 16 drugs targeting the same protein (IGF-1R)4 across 183 clinical trials involving 12,000+ patients. Despite a staggering $1.6 billion spent, none got the green light for oncology use. The root cause (according to the paper)? Shaky pre-clinical evidence. The takeaway? Sharpen the decision criteria when advancing drugs from labs to trials.

One of the potential sources of inefficiency in the biopharma sector is downstream of the fact that drugs have such long development timelines, which are seen as unusual by those working in other industries. Although the total amount of time it takes for a compound to go from identification to approval varies a lot, a commonly cited median figure is 10-15 years. But humans (and their ambitions) operate on shorter timelines. This misalignment can lead employees to push assets that boost their careers in the short-term, even if those assets don't benefit the company or patients in the long run. After all, a drug's real results might only surface a decade later! Roivant aims to solve this by creating equity incentives to align the interests of the Vant's leadership team with the broader goals of Roivant and, ultimately, the success of the Vant. Another way in which they hope to increase efficiency is by using enhanced data analytics tools to pick the right programs; Probably even more crucially, they want to make use of their relationships within biopharma that give them access to a wide range of potential assets to acquire.

The idea of creating an entity that takes advantage of the inefficiency of pharma and makes use of better decision tools/ better business model is interesting and got me quite excited.

However, I was a bit deflated upon finding that for their successfull assets so far, Roivant does not really improve decision making at the level that is most important: Preclinical to Clinical5. Indeed, all of the selected assets in their S-1 filing had already shown some promising Clinical-stage results at the time they were in-licensed. For example, their most recent FDA-approved drug, Tapinarof, was purchased from GSK in 2018, after it had already gone through several promising Phase I and Phase II trials.

I think that aiming to improve decision making at the Preclinical step would have been a much more impactful endeavour. Want a game-changer in drug discovery? Focus on improving decisions at the preclinical stage, the industry's major bottleneck with a stark 1:50 success ratio. Indeed, Scannell’s research that I talked about above mostly focuses on improving decision making at this stage. As for Roivant, they've side-stepped this challenge, sourcing assets already showing promise in clinical trials. These assets already have a higher 1:5 success ratio. Essentially, they're fishing in richer waters.

Still, any improvement is good! If they manage to bring to market successful drugs that would have otherwise been dropped, it makes the entire market more efficient. Side note: For those interested in innovation economics, Roivant could be the ideal study. Carefully Analysing their success rates could reveal the real value of perfecting decisions at the Clinical stage. How much juice can we really get from that squeeze?

Strategy in practice: Axovant

One of the most (in)famous endeavours of Roivant is Axovant. Axovant, one of Roivant’s subsidiaries, faced significant setbacks when its much-hyped Alzheimer's drug, intepirdine, failed in late-stage clinical trials. It didn’t help that not long before these negative results were announced, Axovant had gone through the biggest biotech IPO of the year.

So what happened there?

Building upon their thesis of “rescuing assets” they considered promising, Roivant licensed an Alzheimer’s drug from GSK (interpirdine), through its subsidiary Axovant. The drug had already failed 4 Phase III clinical trials. At this stage one might ask: What were they thinking, trying to “rescue” such a drug? Well, at the time they noticed that this drug showed a small but statistically significant effect on some relevant co-primary end-points6 at a high dosage (35mg) in the case of short term-administration. However, in the larger trial that Axovant carried out after licensing the asset, the results were negative. To quote from the results: “there was essentially no difference between the intepirdine and placebo arms in change from baseline in activities of daily living”.

At the time a lot of leading figures expressed skepticism around Axovant and many saw it as an endeavour doomed to fail, that investors had been lured into due to massive hype. Indeed, here is Derek Lowe commenting abt this in 2016. The rather poor chances of success of this drug can also be glimpsed from the very little amount of money GSK agreed to in order to part ways with the asset: just $5mn. Despite this, some investors (mostly non-biotech ones) were clearly optimistic abt the potential of this asset. Axovant filed for an initial public offering that raised $315mn in the largest biotech flotation on record, securing a valuation of $3bn after the first day of trading. Ramaswamy himself seems to have made $39mn from this deal.

Obviously, the disappointment after the eventual failure of the trials was significant, especially given the “warnings’ from several experienced drug developers. Yet, the pessimistic predictions in the wake of the IPO must NOT be considered an act of particular clarvoyance: Alzheimer’s is such a hard area to operate in, that betting something will fail is always the “safe bet”. A defender of Axovant could say: someone’s gotta try things, especially in risky areas like this! (man in the arena etc etc.)

Still, we have to consider the counterfactual: in a world of limited resources all this money could have been spent on a “low probability of success but still higher than that of interpirdine“ drug, with a presumably higher expected value. But, ultimately, if one thinks this was a misallocation of funds, it’s the investors who are to blame: all the information about the prospects of this drug was available. As for the let-down of the patients and their families that others have invoked: the entity on whom responsibility ultimately lies is the FDA, who agreed with the trial design.

Subsequent successes

Something I have noticed in the online conversation is people seem to focus a lot on Axovant, to the detriment of subsequent successes. After the Alzheimer’s flop, Roivant underwent significant restructuring, which, with the benefit of hindsight, was probably a good idea.

To date, Roivant has had some good results on several indications, including 5 FDA-approved drugs. Most recently, they have gotten an FDA approval for their psoriasis drug Tapinarof, which they are also commercialising. This is the first topical therapy for plaque psoriasis in the last 25 years.

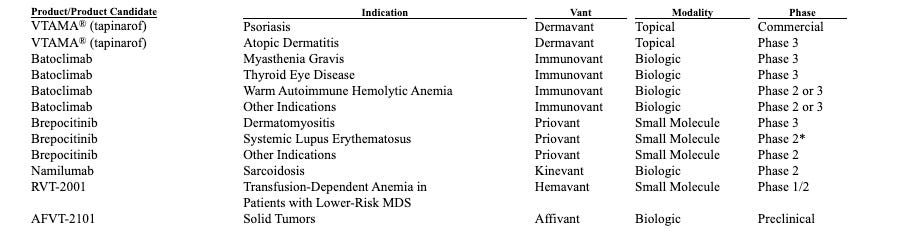

This is a table of selected assets taken from their S-1 filing. Looking at the 11 indications for these compounds something stands out: all but 2 are autoimmune or chronic inflammatory diseases. This is a growing market due to the increasing incidence of Autoimmune disease; It’s also a market that has been relatively less exploited than classic therapeutic areas like oncology.

Another promising asset not included is a monoclonal antibody targeting TL1A in Chron’s disease (via their subsidiary Telavant). Inflammatory bowel disease (Chron’s disease) is an approximately $17 billion market in the United States alone and growing. Another one of Roivant’s subsidiaries, Myovant, was acquired for $1.7 billion in Early 2023 by Sumitomo Pharma. Myovant was focused on women’s health, an underserved area, and prostate cancer. Their most advanced asset was relugolix, which was approved by the FDA in 2020 for the treatment of prostate cancer.

So I think this string of approvals/successes makes it a huge stretch to call Roivant a “scam”. It is a legitimate company that has brought drugs to market after an initial failure. One of its subsidiaries was considered successful enough to be bought by another, more established biopharma company. Unlike the investors behind Axovant’s IPO, they are presumably more knowledgeable about the biopharma industry. As to the extent to which implementing Roivant’s model would actually increase the efficiency of the pharma industry, this is a much harder question to answer. It would require a careful analysis of the counterfactuals for each drug; understanding why the companies that developed them decided to part ways with them & so on.

Conclusion

Overall I think a fair presentation of Roivant should include the successes along its failures. In an industry with such low probability of success as pharma, it seems unfair to focus on one particular asset that failed. I think it will be another few years before we can actually judge what the impact of Roivant has been.

Yet, we must also be cautious about overly-inflated claims of “revolutionising the pharma industry”. A true revolution will come from those who will be able to actually move the needle on the success of Pre-Clinical → Clinical!

Of course, this is a bit of a simplification, as some of Roivant’s spin-offs are also pursuing new technologies. However, at the moment, none of their succesfull candidates have been developed in-house as far as I can tell.

Most biotech start-ups have names that remind of the science/core tech they are based on

In pharmaceutical parlance, an "asset" typically refers to a product, molecule, or technology that has potential therapeutic value or utility in the drug development process. It can be at any stage of research and development, from early-stage discovery to late-stage clinical trials or even marketed products. For example a drug candidate is considered an “asset”

Think of the "target" as the goal in a game, and the "asset" as the equipment or tools you use to score or achieve that goal. In drug development, the goal (target) is to treat a disease by influencing a specific molecule or pathway, and the tools (assets) are the drugs or technologies used to achieve that therapeutic effect.

In essence, preclinical involves lab and animal testing, while clinical involves phased human trials.

The motivation for Axovant’s attempt to “revive” this drug seems to be the small but statistically significant effects in the AZ3110866 trial. The effects seem to have been small enough for GSK to have considered it a “failed” trial.

I worked for Roivant for about two years. They have been working since around 2020 on developing their own pipeline (rather than in-licensing), so the pre-clinical work is not off their radar, it is just hard. See the efforts of Proteovant and VantAI (targeted protein degradation), Psivant (computational drug discovery, descended from Silicon Therapeutics, which Roivant acquired in 2021), and Covant (covalent inhibitors).

In-depth piece. Appreciate it👍